In Italy, the growth of Discount is mainly favored by the growth of fresh products

In August, the fresh products categories increased sales compared to the same period in 2019, mainly due to a sales format.

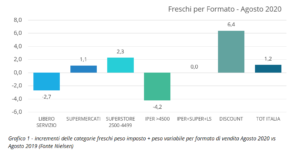

Fresh products, both imposed and variable weight, grew by 1.2% in August compared to the same period in 2019, which is less than proportional to the growth in retail sales as a whole. It should, however, be specified that the figure is an average figure resulting from the overall performance of the various sales formats: in detail, the discount store grew by increasing by +6.4% over the same period in 2019, followed by superstores with +2.3% and supermarkets with +1.1%.

The contraction has instead involved the turnover of the free service (-2.7%) and even more strongly that of the hyper (-4.2%).

In practice, if we were to consider the sales of supermarkets, hypermarkets, and free service the result would be that of parity over the previous year, the leap forward was determined by the strong push that discounters are bringing to the macro category.

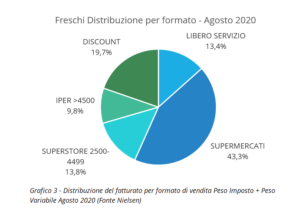

The convenience format is growing, gaining market share on direct competitors and fresh products are one of the main drivers of this evolution. In practice, considering 100 sales of fresh products in the entire mass-market retail, the supermarket channel occupies over 43% of sales, so roughly the share that this format has in the overall stores.

However, 19.7% of total sales are produced by discount stores, which means that the national market share and that of fresh products are perfectly in line, so the incidence achieved by traditional channels between sales by imposed weight and those by variable weight are equaled by discount stores that do not make use, for the most part, of the served counters. Following the free service is worth 13.4%, the superstore 13.8%, and the hyper 9.8%.

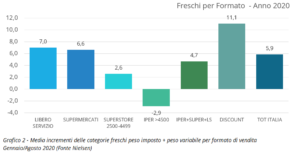

In view of the above, as expected, the first eight months of the year generated a significant increase in sales in all categories of fresh products. Inflation certainly supported this trend, but the growth was and still is generated by the events we experienced and this is nothing new.

In the first eight months of 2020, fresh products, in the total sales formats, grew by +5.9%. There was a resounding increase in discount stores with +11.1%, but also free service (+7%) and super (+6.6%) grew strongly, and the superstore format also achieved a good increase, equal to +2.6%. It is clear that the IPER with a decrease of -2.9% is now objectively suffering and despite this contraction, the hyper+super+free service formats as a whole grew by +4.7%.

The individual categories

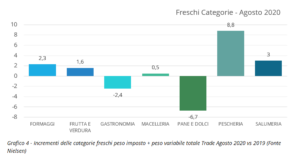

Within the individual categories in August, the strong increase of the fish product sales with +8.8% stood out. The delicatessen grew by +3%, cheese by +2.3%, fruit and vegetables by +1.6% and even if slightly, the butchery with +0.5%.

There was a sharp contraction in bread and sweets (-6.7%) as well as gastronomy (-2.4%). These last two categories have suffered since the beginning of the year, in fact, the former, in the performance comparison 2020 vs. 2019 in the first eight months of the year, lost -8.4% and the latter -6.1%.

2020, also due to inflation in the first six months of the year, saw great increases in sales in the categories of cheese with +10.2%, butchery with +8.2%, fruit and vegetables with +6.7% and seafood and delicatessen with +6.5%.

As a result of these dynamics, today fruit and vegetables account for 30% of sales of all fresh and very fresh products, butchery for 22.1%, cheeses for 17.8%, delicatessen for 15.8%, bread and cakes for 6.2%, gastronomy for 4.1% and seafood for 4%.